- Story

“A high-performing healthcare system is very expensive”

03.04.2024 In early June, the Swiss people will vote on two initiatives on health insurance premiums. How bad is the state of Switzerland’s healthcare system? Tobias Müller, a healthcare economist at BFH, gives a double diagnosis in our interview.

Health insurance premiums have been rising for many years. How bad is the state of Switzerland’s healthcare system?

It is in a poor state in some ways, but perfectly healthy in others. First of all, I will say it is healthy because we have a highly effective healthcare system in Switzerland. Our life expectancy has risen sharply over the past century from around 68 to over 84 years of age. We are no longer dying of infectious diseases and a cancer diagnosis often does not mean imminent death nowadays. However, a very sophisticated, high-tech system is expensive.

The ‘sick’ part of the healthcare system is its inefficiency in many different areas. The system provides misplaced incentives. For example, outpatient remuneration is structured in a way that allows service providers to charge for every service individually. That means the more services they provide, the more they can bill for. That inevitably results in oversupply.

By international standards, we also have a very high density of hospital beds, doctors, and medical equipment such as X-ray machines. Despite the constant debate over the care crisis, that is true of the care sector too. There are more than 18 care staff for every 1000 inhabitants in Switzerland. By comparison, that figure is 12 in the USA, Germany and the Netherlands. Maintaining this kind of system is extremely expensive. Outstanding medical services could still be provided with a more streamlined structure.

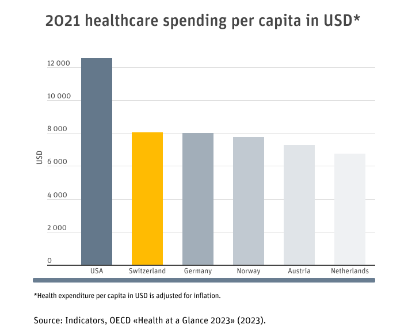

What are Switzerland’s healthcare costs like compared with other countries?

In terms of healthcare spending, Switzerland is in second place globally behind the USA. Healthcare costs per capita are just over $12,500 in the USA, while they stand at around $8,000 in Switzerland and Germany. They are followed by Norway at over $7,800. In terms of cost contributions by policyholders, Switzerland comes out top globally at around $1,600 per capita. The average for the OECD states is around $700. Residents pay more in Switzerland than in any other country.

It is said that the more often people visit their doctor, the more premiums rise. Is that true?

That is correct technically speaking. The more GP consultations there are, the higher the healthcare costs and in turn the premiums will be. But do not forget: we all have to cover costs ourselves of at least CHF 300 each year. So that is around two consultations that do not cost the system anything. The demand for services is also growing because people are living longer and, as a result, suffering more from chronic illnesses.

Residents spend more on healthcare costs in Switzerland than in any other country.

What impact do medical progress and our ageing society have on premiums?

Over the past five years, total annual costs have risen by around CHF 10 billion to CHF 90 billion. Much of this increase is due to medical progress and the resulting extended range of services. Demographic development in Switzerland also has an impact on costs as older people now require more medical services than younger ones on average.

One of the two initiatives proposes limiting the share of income that people have to spend on health insurance premiums to 10%. How high is the share of income spent on premiums on average and how many people spend over 10%?

Over the past 20 years, average premiums have risen by 105%, while salaries have only increased by around 21%. This means that an ever-greater share of income is being spent on premiums. On average, around 7% of disposable income is spent on health insurance premiums. Twenty years ago, it was around 4%. Just under two-fifths of the population now spend between 10 and 20% of their disposable income on health insurance premiums. That represents a sizeable share of the Swiss population – and is an alarmingly high level.

How many people are now unable to pay their premiums and are reliant on state-supported reductions?

Over a quarter of people in Switzerland now get a reduction on their premiums. The average level of discount depends on the canton of residence and varies significantly. While some cantons cover up to 70% of annual premium costs, policyholders in other cantons still have to pay over 50% of premiums themselves despite the reduction.

Two initiatives on health insurance: it’s all about health insurance premiums

On 9 June 2024, the Swiss electorate will vote on two popular initiatives concerning health insurance:

Premium Relief Initiative

The ‘Premium Relief Initiative’ proposes limiting the amount policyholders have to spend on premiums to 10% of their disposable income. If total premium costs exceed that level, policyholders would be entitled to a discount.

The Swiss Parliament has adopted an indirect counterproposal to the ‘Premium Relief Initiative’.

Cost-Brake Initiative

The ‘Cost-Brake Initiative’ calls on the federal government to implement measures if the rise in average annual health insurance costs per person exceeds one fifth of the nominal wage trend.

Parliament has also adopted an indirect counterproposal to the ‘Cost-Brake Initiative’.

What would the 10% premium limitation mean for the healthcare system?

Limiting premiums to 10% of disposable income does not affect healthcare costs directly. Low-income households would simply be less heavily burdened by premium costs. The federal government or the cantons would presumably have to meet those costs instead. This is not expected to result in savings for the healthcare system or an increase in costs. It would not resolve the structural problems of over-supply. Nor is there any reason to assume people would consult their doctor more often just because they are paying less for the service.

In response to the other initiative, politicians have set cost and quality targets in the Health Insurance Act. What does that mean for policyholders and service providers?

Cost targets may have an impact on service providers. If, for example, they receive flat-rate remuneration for a service and have to cover the costs of anything exceeding that themselves, then they would think twice about which examinations and treatments they wish to carry out on patients. Cost and quality goals may represent a step in the right direction. However, the key factor is how they are implemented. In my view, there are still too many unanswered questions to predict the potential effect.

On average, around 7% of income is spent on health insurance premiums. Twenty years ago, it was around 4%.

What other options are there to curb rising premium costs?

Shifting services more towards a flat-rate contributions model is one promising approach. Service providers would then receive a fixed amount for a person’s treatment. The Netherlands – which has a similar healthcare system to Switzerland’s – has had positive experience with a flat-rate contribution and supplementary payments for services for chronically ill patients.

I also believe savings could be made on medical services that have little impact. One example of what is called low-value care is testing for vitamin-D deficiency. This kind of testing costs just under CHF 50.–, whereas a prescription for a Vitamin D supplement costs less than CHF 5.–. Most people get enough vitamin D through a balanced diet and regular sunlight. Treatment with a vitamin D supplement does not last long enough to justify the costs of testing. Savings could be made on services like this testing without compromising medical standards.

Tobias Müller

Tobias Müller is a Professor of Health Economics and Head of the Empirical Health Economics team at the Institute of Health Economics and Health Policy of BFH’s School of Health Professions. In addition to health economics, his specialist fields include causal analysis, machine learning and randomised controlled studies used as models in medical research.

Category: Story